Welcome readers, and thanks for subscribing! The Altcoin Roundup newsletter is now authored by Cointelegraph’s resident newsletter writer Big Smokey. In the next few weeks, this newsletter will be renamed Crypto Market Musings, a weekly newsletter that provides ahead-of-the-curve analysis and tracks emerging trends in the crypto market.

The publication date of the newsletter will remain the same, and the content will still place a heavy emphasis on the technical and fundamental analysis of cryptocurrencies from a more macro perspective in order to identify key shifts in investor sentiment and market structure. We hope you enjoy it!

DeFi has a problem, pump and dumps

When the bull market was in full swing, investing in decentralized finance (DeFi) tokens was like shooting fish in a barrel, but now that inflows to the sector pale in comparison to the market’s heyday, it’s much harder to identify good trades in the space.

During the DeFi summer, protocols were able to lure liquidity providers by offering three- to four-digit yields and mechanisms like liquid staking, lending via asset collateralization and token rewards for staking. The big issue was many of these reward offerings were unsustainable, and high emissions from some protocols led liquidity providers to auto-dump their rewards, creating constant sell pressure on a token’s price.

Total value locked (TVL) wars were another challenge faced by DeFi protocols, which had to constantly vie for investor capital in order to maintain the number of “users” willing to lock their funds within the protocol. This created a scenario where mercenary capital from whales and other cash-flush investors essentially airdropped funds to platforms offering the highest APY rewards for a short period of time, before eventually dumping rewards in the open market and shifting the investment funds to the greener pastures.

For platforms that secured series funding from venture capitalists, the same sort of activity took place. VCs pledge funds in exchange for tokens, and these entities reside in the ranks of the largest tokenholders in the most lucrative liquidity pools. The looming threat of token unlocks from early investors, high reward emissions and the steady auto-dumping of said rewards led to constant sell pressure and obviously stood in the way of any investor deciding to make a long investment based on fundamental analysis.

Combined, each of these scenarios created a vicious cycle where protocol TVL and the platform’s native token would basically launch, pump, dump and then slip into obscurity.

Rinse, wash, repeat.

So, how does one actually look beyond the candlestick chart to see if a DeFi platform is worth “investing” in?

Let’s take a look.

Is there revenue?

Here are two charts.

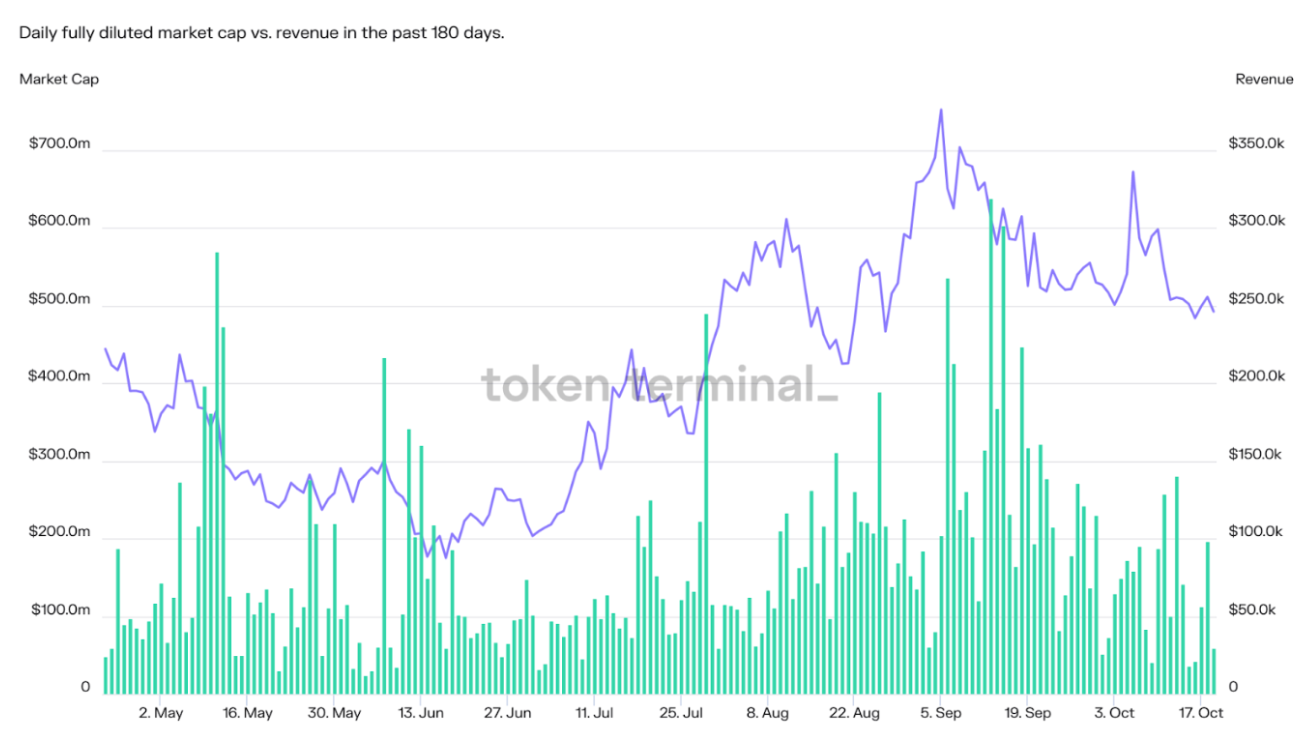

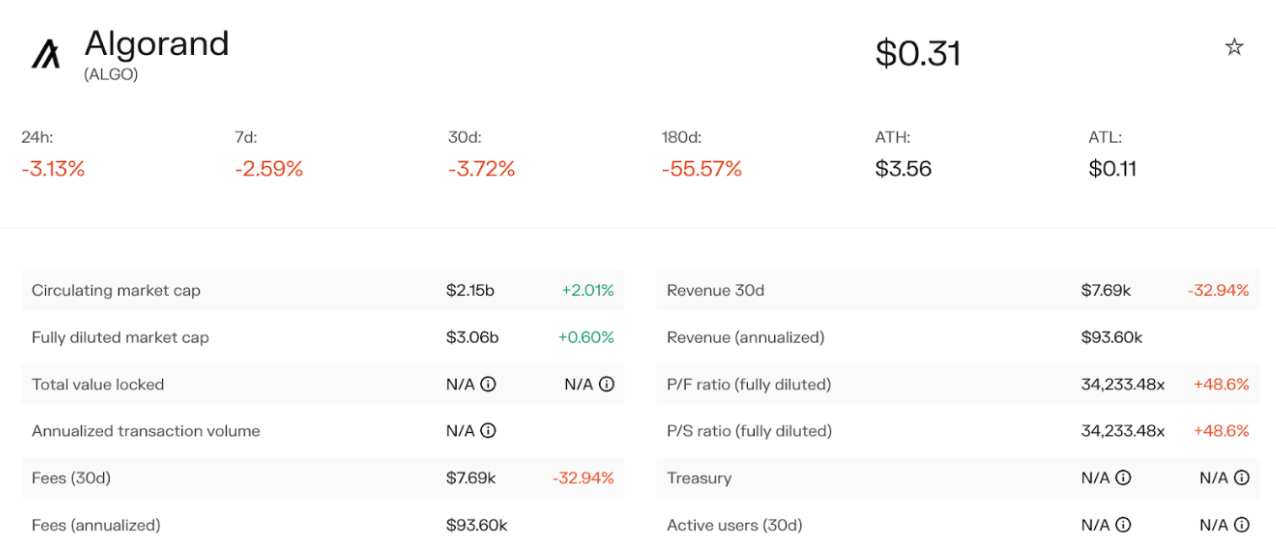

Yes, one is going up and the other is going down (LOL). Of course, that’s the first thing investors look for, but there’s more. In the first chart, one will notice that Algorand (ALGO) has a $2.15-billion circulating market cap and a fully diluted market cap of $3.06 billion. Yet its 30-day revenue and annualized revenue are $7,690 and $93,600, respectively. Eye-raising, isn’t it?

Circling back to the first chart, we can see that while maintaining a $2.15-billion circulating market cap and supporting a wide ecosystem of assorted decentralized applications (DApps), Algorand only managed to produce $336 in revenue on Oct. 19.

Unless there’s something wrong with the data or some metrics related to Algorand and its ecosystem are not captured by Token Terminal, this is shocking. Looking at the chart legend, one will also note that there are no token incentives or supply-side fees distributed to liquidity providers and token stakers.

Related: 3 emerging crypto trends to keep an eye on while Bitcoin price consolidates

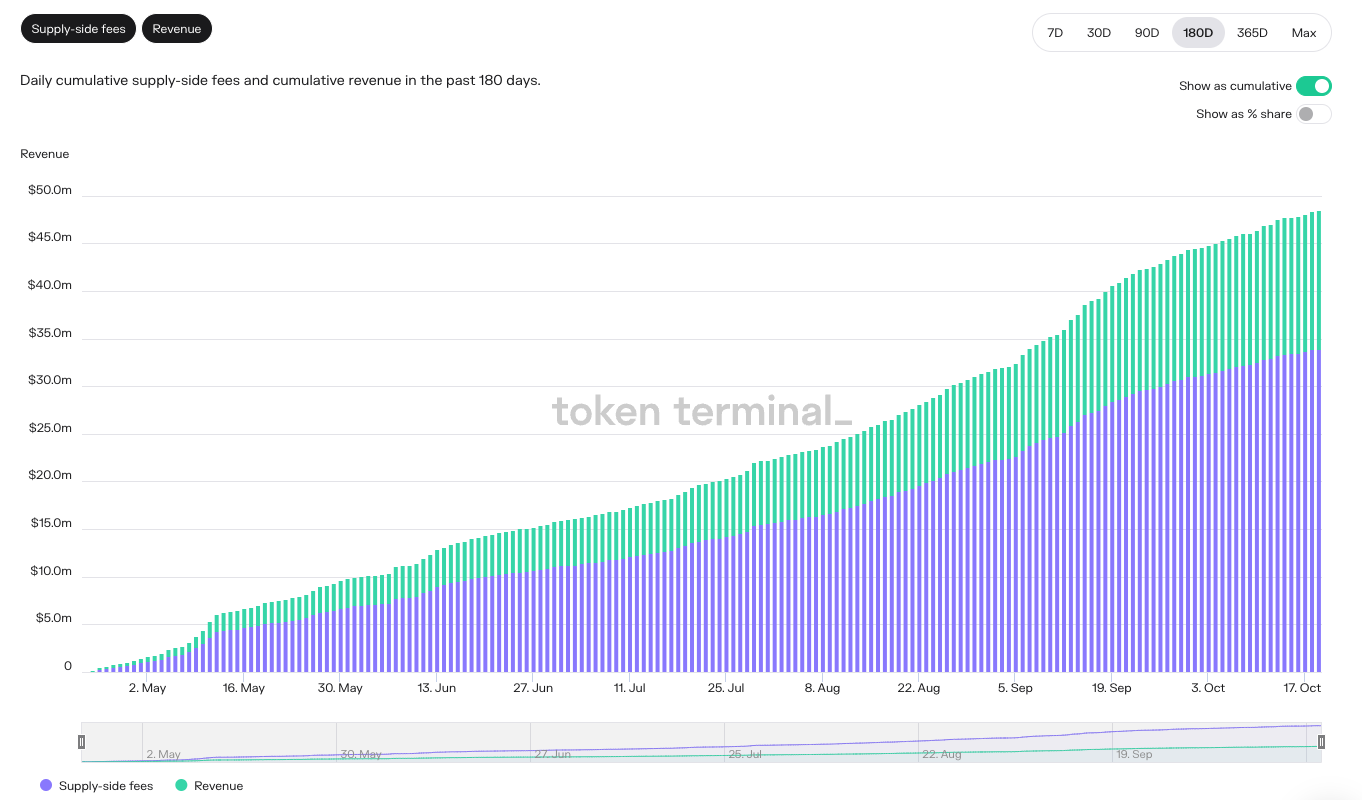

GMX, on the other hand, tells a different story. While maintaining a circulating market cap of $272 million and an annualized revenue of $28.92 million, GMX’s cumulative supply-side fees have steadily increased to the tune of $33.9 million since April 24, 2022. Supply-side fees represent the percentage of fees that go to service providers, including liquidity providers.

Issuance and inflation

Before investing in a DeFi project, it’s wise to take a look at the token’s total supply, circulating supply, inflation rate and issuance rate. These metrics measure how many tokens are currently circulating in the market and the projected increase (issuance) of tokens in circulation. When it comes to DeFi tokens and altcoins, dilution is something that investors should be worried about, hence the allure of Bitcoin’s (BTC) supply cap and low inflation.

As shown below, compared to BTC, ALGO’s inflation rate and projected total supply are high. ALGO’s total supply is capped at 10 billion, with data showing 7 billion tokens in circulation today, but given the current revenue generated from fees and the amount shared with tokenholders, the supply cap and inflation rate don’t inspire much confidence.

Before taking up a position in ALGO, investors should look for more growth and daily active users of Algorand’s DApp ecosystem, and there obviously needs to be an uptick in fees and revenue.

Active addresses and daily active users

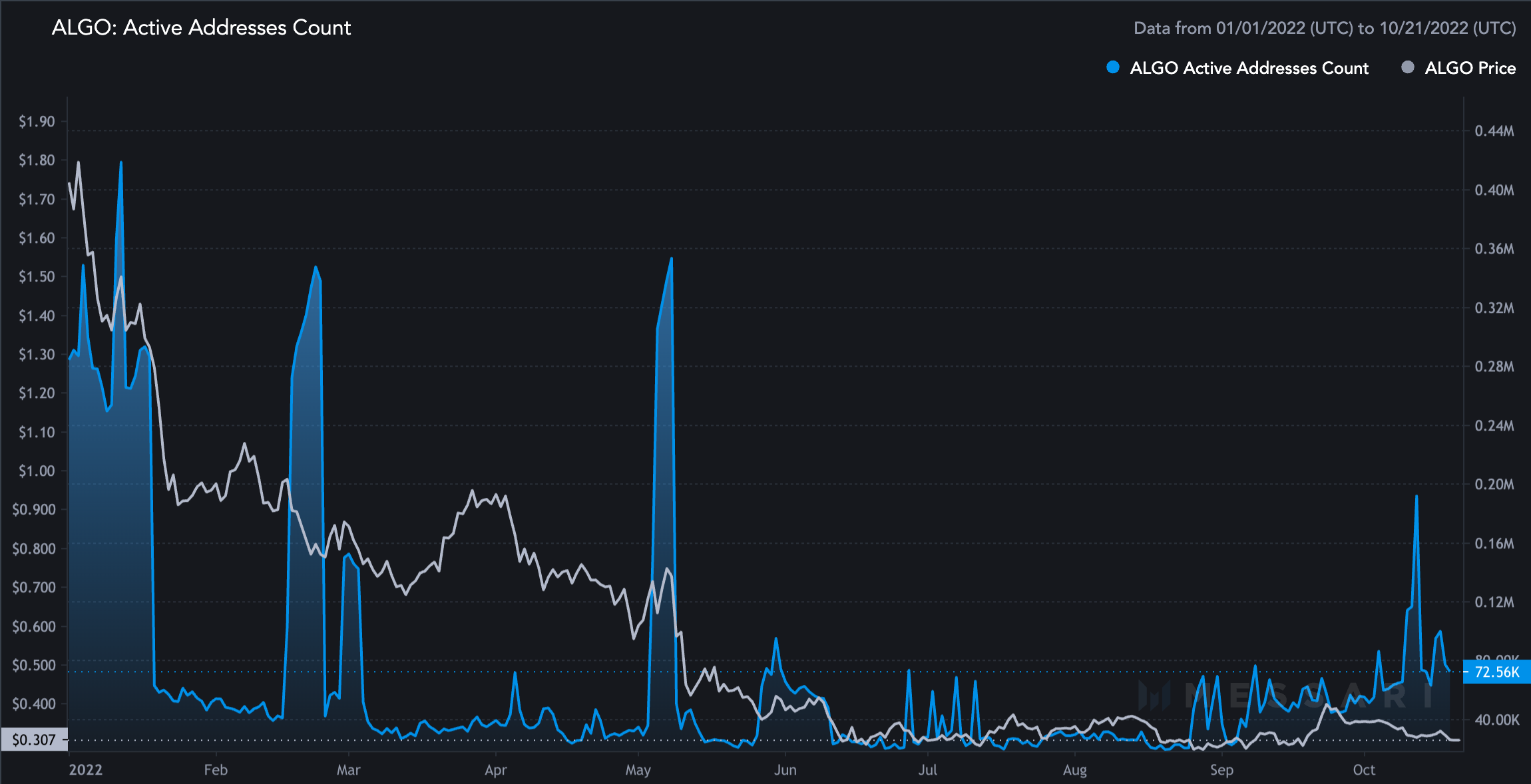

Whether revenues are high or low, two other important metrics to check are active addresses and daily active users if the data is available. Algorand has a multi-billion-dollar market cap and a 10-billion ALGO max supply, but low annual revenue and few token incentives present the question of whether the ecosystem’s growth is anemic.

Viewing the chart below, we can see that ALGO active addresses are rising, but generally, the growth is flat, and active address spikes appear to follow price surges and sell-offs. As of Oct. 14, there were 72,624 active addresses on Algorand.

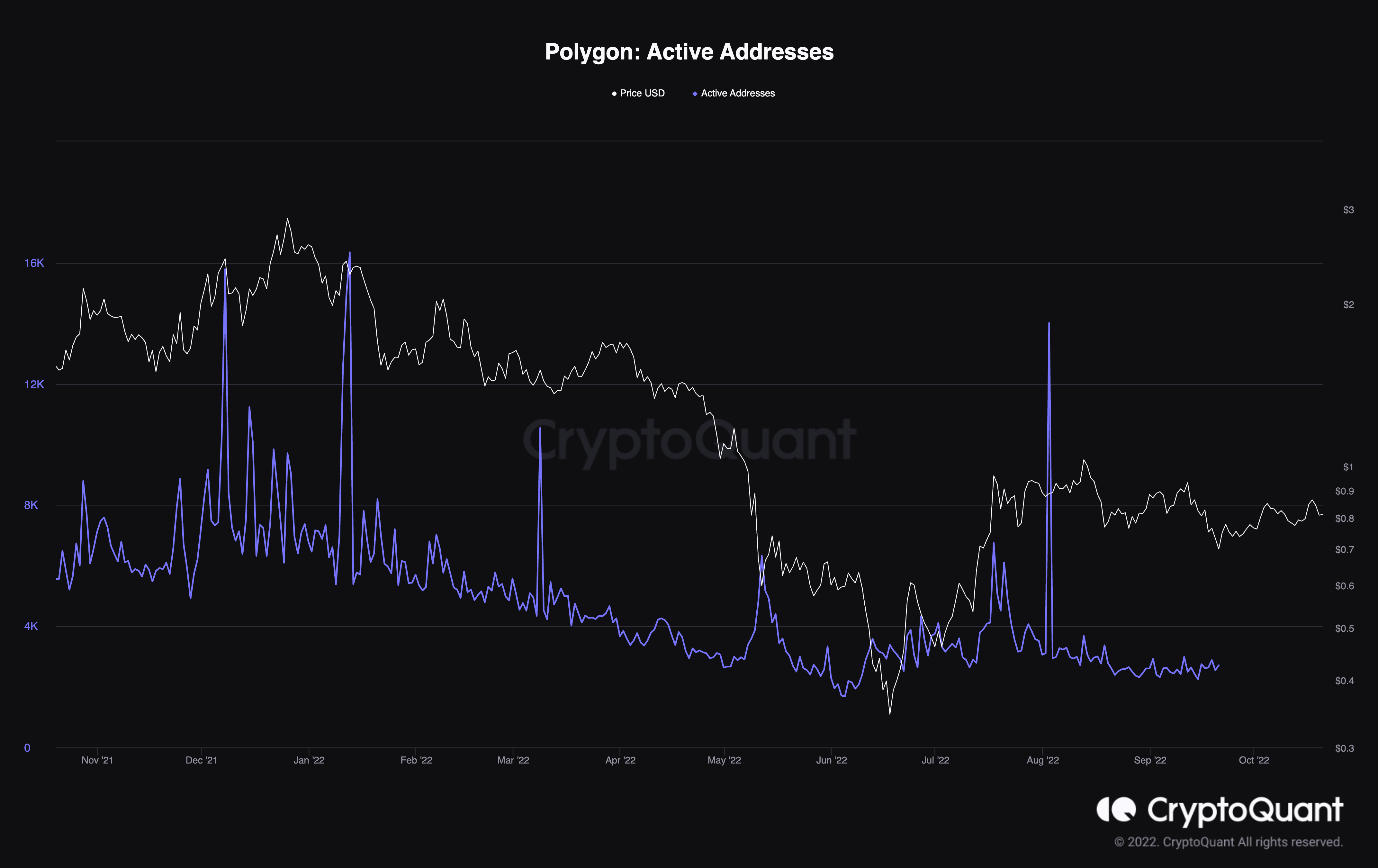

Like most DeFi protocols, the Polygon network has also seen a steady decline in daily active users and MATIC’s price. Data from CryptoQuant shows 2,714 active addresses, which pales in comparison to the 16,821 seen on May 17, 2021.

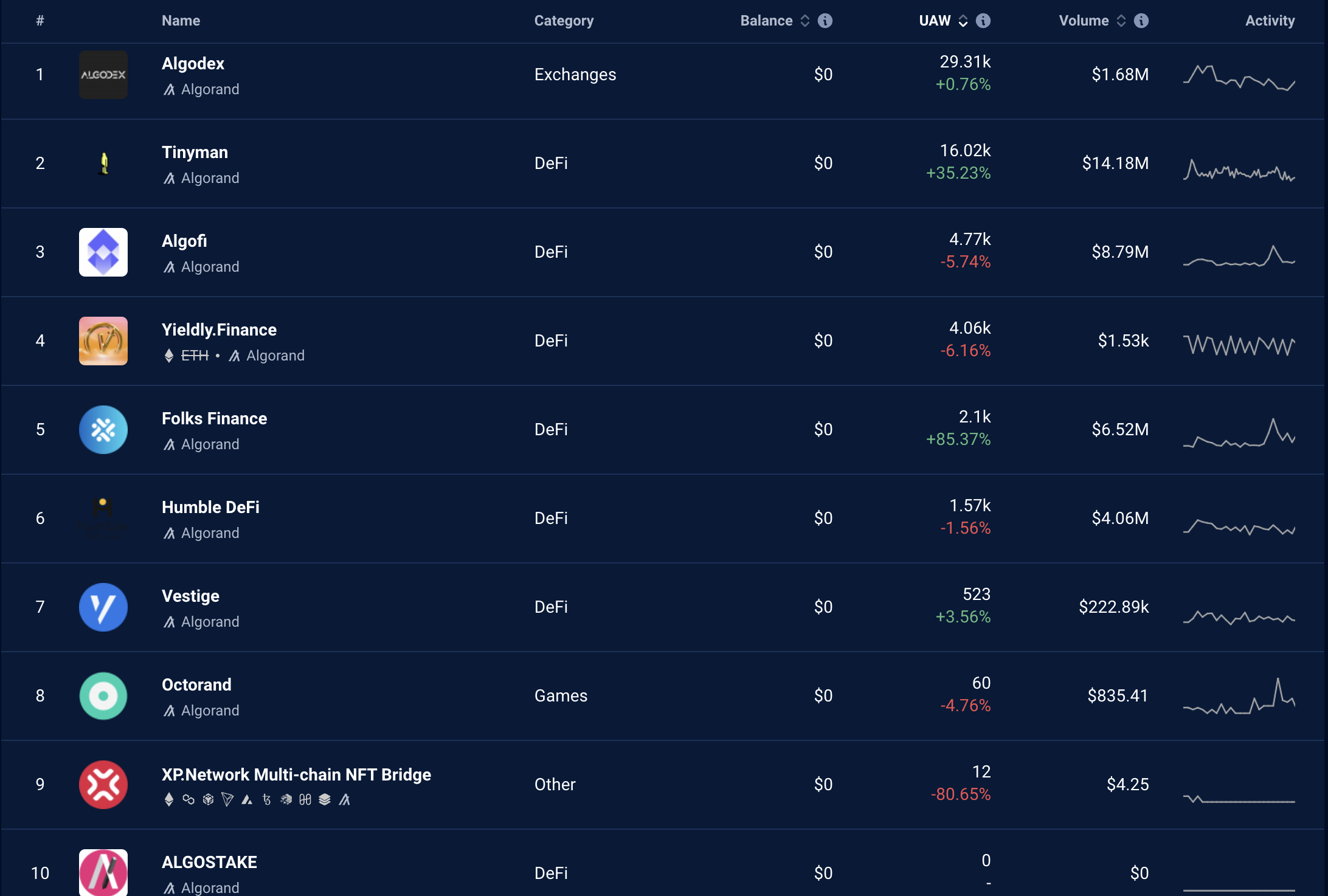

Still, despite the decline, data from DappRadar shows a good deal of user activity and volume spread across various Polygon DApps.

The same cannot be said for the DApps on Algorand.

Right now, the crypto market is in a bear market, and this complicates trading for most investors. At the moment, investors should probably sit on their hands instead of taking kiss-and-a-prayer moon shots at every small breakout that turns out to be bull traps.

Investors might be better served by just sitting on their hands and tracking the data to see when new trends emerge, then looking deeper into the fundamentals that might back the sustainability of the new trend.

This newsletter was written by Big Smokey, the author of The Humble Pontificator Substack and resident newsletter author at Cointelegraph. Each Friday, Big Smokey will write market insights, trending how-tos, analyses and early-bird research on potential emerging trends within the crypto market.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph.com. Every investment and trading move involves risk, you should conduct your own research when making a decision.

Be the first to comment